The survey shows average growth of 2.0% q4/q4, not far from June SEP at 2.1% (unchanged from March).

Figure 1: GDP (bold black), May Survey of Professional Forecasters median (blue), FT-Booth School mean (tan square), Survey of Economic Projections/FOMC June median suggested (light green x), GDPNow of 7 Jun suggested ( sky blue square ), all in bn.Ch.2017$ SAAR. Source: BEA 2024Q1 second release, Philadelphia Fed, Booth School survey, Federal Reserve Board, Atlanta Fed, and author’s calculations.

While the median is 2.0% 2024 q4/q4, the 10/90 percentile range is 1.8%-2.7%. I was very depressed, between 1.8% (0.8% to 2.5%). The average slope of SEP (lower and upper 3 subtractions) is 1.9%-2.3%, the range (all responses) is 1.4%-2.7%.

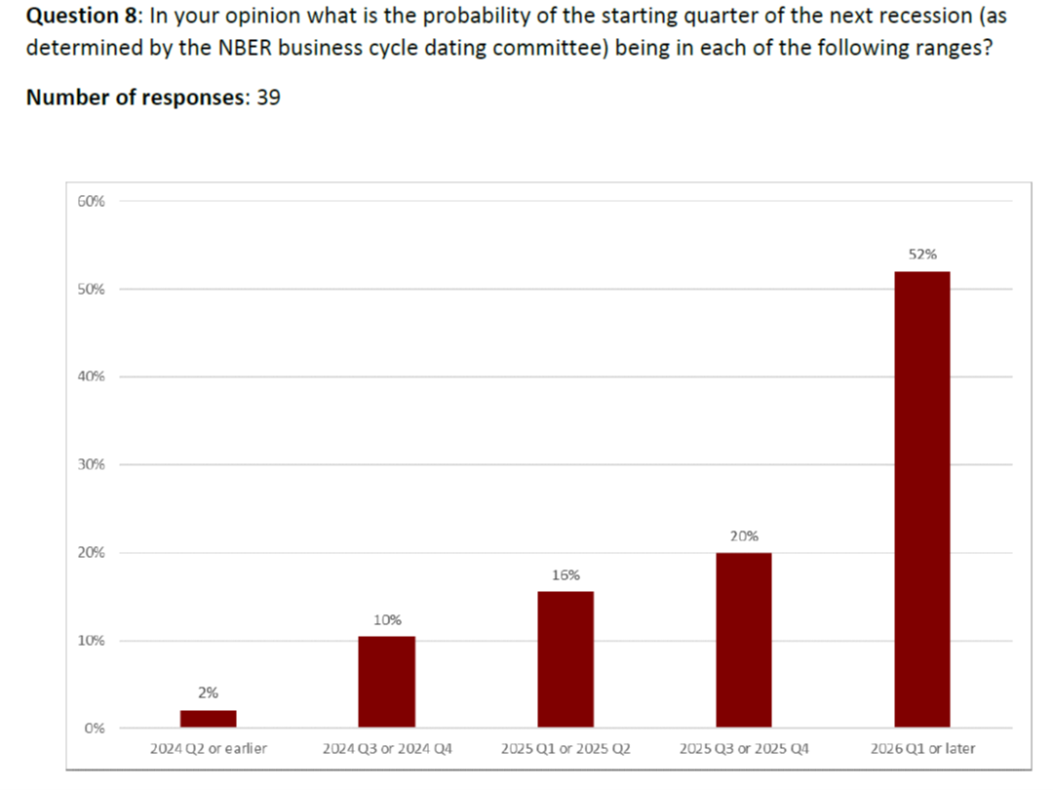

The initial model response for a recession is now 2026Q1 or later, compared to March (see here).

Source: FT-Booth School Survey (June 2024).

The initial probability of a recession in 2024 fell from 18% in March to 12% in May, while the modal forecast for 2026Q1 or later rose from 46% to 52%. Once again, I have a very sad short term, at 40% probability in 2024, which shows the effects of the spread of the name (but we remember the debt service ratio).

FT article here.

Source link