Lamebert here: Whaddaya know.

By Alessandra Bonfiglioli, Professor of Economics (on leave) at Queen Mary University of London, Rosario Crinò, Professor of Economics at the University Of Bergamo, Gino Gancia, Fellow, International Trade and Regional Economics, and Ioannis Papadakis, Research Fellow at the University of Sussex. Originally published at VoxEU.

Harnessing the power of artificial intelligence has become one of the top priorities for policy makers around the world. However, doing so first requires a thorough understanding of the effects of these technologies on the labor market. Using data from all US destinations over the period 2000-2020, this column presents evidence that the adoption of AI has reduced employment, except for high-paying jobs and those requiring degrees in STEM subjects.

Artificial intelligence (AI) is often viewed as one of the most transformative and disruptive technologies of recent times (see original Vox columns by Baldwin 2018 and Bughin 2017). Thanks to the development of machine learning techniques and the growing availability of large amounts of digital data, the last twenty years have seen a significant increase in the use of AI systems, including web search engines, targeted advertising, recommendation systems, productivity or creative tools. , and chatbots. A pressing policy question is how these developments will affect labor markets and employment in particular. On the other hand, smart tools promise to improve people’s skills and create new demand for certain skills (e.g. Brynjolfsson et al. 2023, McKinsey Global Institute 2017). On the other hand, AI may bypass workers in decision-making tasks and make them redundant, or it may fuel automation (Acemoglu 2022, Acemoglu and Johnson 2023). Whether AI will complement or replace workers is therefore an important question, for which there is still little systematic evidence.

In a recent work (Bonfiglioli et al. 2023), we study the employment impact of the first phase of AI adoption, using variations across US Commuting Zones (CZs) over the period 2000-2020. We take a broad definition of AI as algorithms applied to big data, the spread of which started in the early 2000s and accelerated after 2010. Although our sample predates the development of large linguistic models such as ChatGPT, it nevertheless includes the rise of the digital economy and all major companies involved in the collection of big data, such as Amazon, Google, and Facebook.

Measuring AI Adoption Across US Transportation

Our analysis faces two challenges. The first is that the adoption of AI is difficult to measure, as there are no official statistics available so far. However, the use of AI technology requires employees with special programming skills. Using a novel section of the O*NET database – “Hot Technologies” – we classify AI-related jobs as those whose job postings often require software used for machine learning and data analysis. Our basic classification of AI-related jobs includes 19 titles, such as data scientists, computer programmers, software developers, and web designers. Then we find out Adoption of AI from the growing relative importance of these AI-related activities. A second challenge in identifying causal effects is that AI adoption may be associated with other shocks that may affect employment. To overcome this problem, we use the shift-share tool, AI exposurewhich includes US industry-level AI acquisitions and CZ-level pre-employment shares across industries. This allows us to identify the CZs most exposed to AI as those specialized in industries that have experienced the fastest growth in AI-related jobs across the country.

Between 2000 and 2020, the employment share of AI-related occupations nearly doubled in the US, rising from 0.14% to 0.20%. Most of this increase occurred after 2010. There are significant differences in the spread of AI technology across industries. The adoption of AI has increased significantly in the service sector, especially in advanced branches such as information, services, science and business. It is also important in other services, such as electricity, and in other areas of the public sector, such as national security and international affairs. On the other hand, the adoption of AI is still limited in manufacturing. This feature distinguishes the adoption of AI from the use of industrial robots, which are mainly concentrated in the manufacturing sector (Acemoglu and Restrepo 2020).

Figure 1 presents color maps showing how AI adoption (panel a) and AI exposure (panel b) vary across US CZs, with darker colors representing higher levels of adoption or exposure during the sample period. Negative values are extremely rare (only 6% of CZs), which means that the deployment of AI technology has been widespread in the US for the past two decades. Interestingly, our measure of AI adoption (panel a) works very well in capturing the spread of AI both in expected areas such as Boston, Seattle, and Silicon Valley, and in new high-tech areas such as Boulder, Bozeman, and Salt Lake. The city. Our estimate of AI exposure (panel b) removes variation in AI uptake that may have been driven by contemporaneous CZ level shocks, which could confound the estimate.

Figure 1 Adoption of AI and Exposure to AI in US Travel

The source: US Census and American Community Survey.

Notes: The top map plots the average value of AI adoption rate in each CZ between the decades 2000-2010 and 2010-2020. The map below plots the corresponding values of the AI exposure ratio.

Negative Impact of AI Adoption on Employment

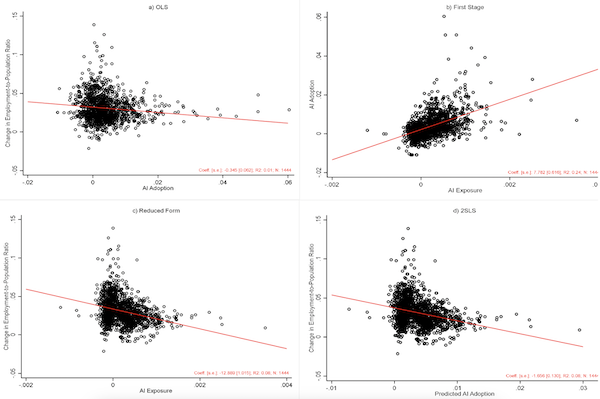

Figure 2 provides a graphical representation of our technical strategy and main results. The dots in each of the four scatterplots represent observations for each CZ and decade (2000–2010 and 2010–2020), while the red line is the linear regression line. Panel a (OLS) documents a negative correlation between AI adoption and the decadal change in the employment rate at the CZ level. Panel b (first section) confirms that exposure to AI is a strong predictor of AI adoption and, thus, a powerful tool for the diffusion of this technology. Panel c (reduced form) shows that exposure to AI is significantly related to employment growth. Finally, panel d (2SLS) plots the relationship between AI adoption, as predicted by AI exposure, and the ten-year change in the employment rate, highlighting a strong negative (causal) effect of AI adoption on employment growth. Overall, these graphs show that CZs specializing in sectors experiencing AI-related employment growth have had strong AI adoption rates, causing them to experience employment declines. On average, our estimates mean that if a CZ with average AI adoption during the hypothetical sample period had no adoption at all, its employment rate would have increased by 0.6 percentage points more.

Figure 2 AI Adoption, AI Exposure and Employment in US Travel

Notes: The measurement sample consists of 722 CZs observed in two decades, 2000-2010 and 2010-2020. For each group, observed is the tenth pair of CZ x. AI adoption predicted by the fitted value of the AI adoption rate from the first stage regression in Plot b).

These results are robust to controlling for additional labor market shocks, such as import competition from China (Autor et al. 2013), the adoption of industrial robots (Acemoglu and Restrepo, 2020), and the increased use of ICT. They also catch on when they use other definitions of AI-related jobs and when they control outsiders in various ways.

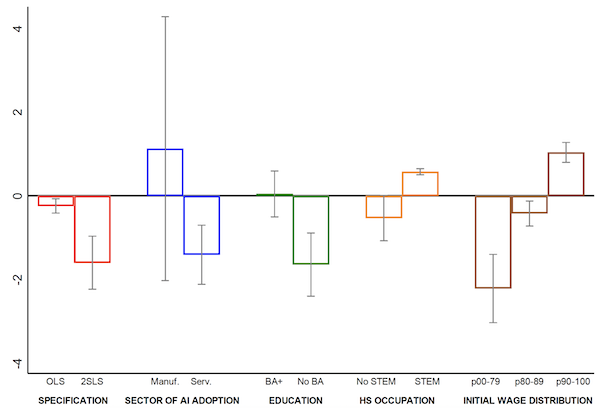

Figure 3 shows how the relationship between AI adoption and job growth varies across factors. The figure reveals three main results. First, the impact of AI adoption is stronger when AI adoption is modeled using AI exposure (2SLS versus OLS specification), suggesting that confounding factors tend to mask the negative impact of AI on employment. Second, the effect of AI is driven by adoption in the service sector, where the deployment of these technologies is most common. Third, workers without a college degree are the most affected by AI adoption. On the other hand, the only workers who will benefit from the adoption of AI are those in jobs that require STEM degrees and those in the top 10% of the income distribution.

Figure 3 Heterogeneity

Notes: The figure reports the estimated coefficients and 90% confidence intervals for the AI acceptance rate from different specifications. The sample size consists of 722 CZs observed in two decades, 2000-2010 and 2010-2020.

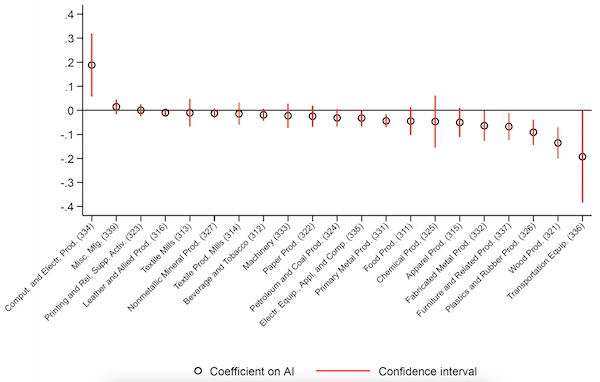

Our results also show that the negative impact of AI adoption is not limited to the service sector but also extends to manufacturing employment, where the use of this technology is still limited. In particular, the manufacturing sector accounts for about 45% of the total impact of AI adoption on employment, compared to 60% for the service sector. To shed light on the underlying mechanism of this disparity, Figure 4 reports the estimated effects of AI adoption on employment in different manufacturing industries. This figure shows that workers in industries characterized by a high degree of automation, such as transport equipment and wood products, are most affected. This suggests that the adoption of AI in services may, in fact, be used to automate tasks in manufacturing.

Figure 4 AI Adoption and Employment in Individual Manufacturing Industries

Notes: The measurement sample consists of 722 CZs observed in two decades, 2000-2010 and 2010-2020.

Conclusions

Recent developments in the field of AI have sparked a lot of talk about the future of work. While no one can predict the exact direction new things and applications will take, we think it’s important to start by understanding the effects these technologies are already having. Our results point to strong negative effects of AI adoption on employment for many workers and sectors. Although more small-scale evidence is needed to identify precisely how these negative effects are manifested, our evidence is nonetheless consistent with the view that AI contributes to changing jobs and increasing inequality.

References are available at the beginning.

Source link